What is a fixed indexed annuity?

When you’re looking for upside potential with downside protection

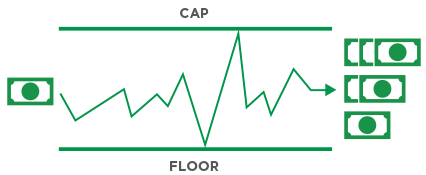

A fixed indexed annuity is a tax-deferred, long-term savings option that provides principal protection in a down market and opportunity for growth. It gives you more growth potential than a fixed annuity along with less risk and less potential return than a variable annuity.

Returns are based on the performance of an underlying index, such as the S&P 500® Composite Stock Price Index, a collection of 500 stocks intended to provide an opportunity for diversification and represent a broad segment of the market. While the benchmark index does follow the market, as an investor, your money is never directly exposed to the stock market.

For more information about fixed indexed annuities, check out our video

What are the benefits?

Annuity resources

Annuities articles

Visit our library of annuities articles in the Learning Center.

Which annuity may be right for you?

Learn about the features and benefits offered by the different annuity types.