What to do during a down market

What a volatile market means

Market volatility refers to when groups of stocks or bonds rapidly change price — up or down — over a relatively short time span.

Lower volatility

is when the price change is slower, less significant and over a longer period.

Higher volatility

is when the price change is faster, more significant and over a shorter period. Rapid price changes can impact the value of your retirement portfolio.

What a bear market means

How the market can affect your retirement portfolio

Whether you're in the midst of a volatile market, a bear market or a recession, the value of your retirement portfolio could be significantly affected. Watching your account total go up and down, or continue to go down temporarily for a period of time, isn't easy. But it's a normal part of investing in the markets. In fact, there have been periods of increased market volatility throughout the long history of the U.S. stock and bond exchanges.

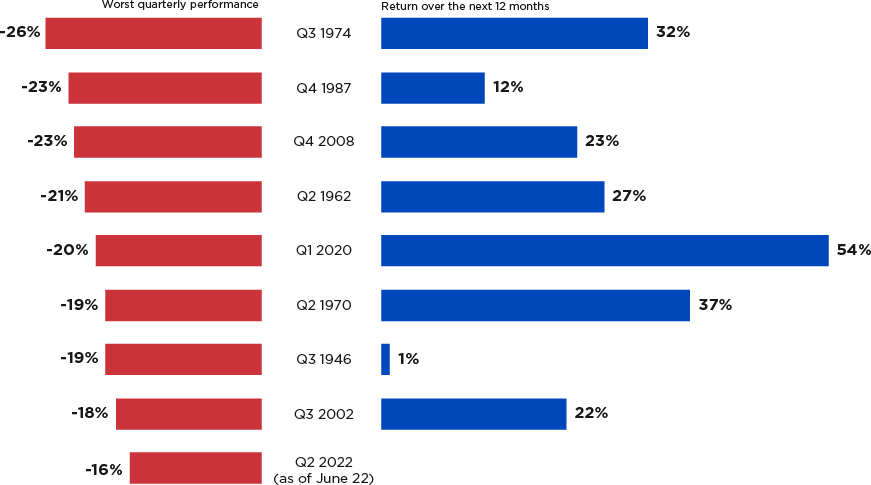

S&P 500® performance after severe quarterly losses 1945 to present

Source for chart data: FactSet Research Systems, Nationwide IMG Competitive Intelligence Team

You may be wondering "But how bad are my losses going to be in this current market?" As the chart above illustrates, the second quarter of 2022 may be the ninth-worst quarter for the S&P 500 Index since World War II. However, in the 12-month periods following down quarters in the past, the benchmark stock index rose by an average of 26%.

This illustrates why investors should ignore short-term market noise and stay focused on their long-term investment strategy.

Tips on what to do in a down market

Refer to these 5 tips before deciding to take action in a down market:

Don't let market fluctuations alone make you change investments. Remember, bad years are generally balanced by good years.

Make sure you temper your expectations for growth. Your asset allocation should be based on return expectations needed to meet certain goals and objectives. If your portfolio includes stocks, down markets are already factored into your long-term return expectations.

By continuing to invest regularly during a down market, you'll often be able to buy more of your chosen investments with the same amount of money as before. Riding out the down market so that you can participate in the rebound should be the goal.

Reviewing your allocations and making necessary changes periodically is smart, but checking too often may lead to hasty decisions that negatively impact your returns.

Don't dwell on how much more your portfolio was worth at the time of its most recent high. Unless you sell investments or withdraw funds, the "losses" are only on paper. Long-term investing historically leaves plenty of time for the market to recover.

Of course, you should always keep in mind that investing involves risk, including the possible loss of principal.