1. Save for retirement

Yes, saving for the future can help you trim today’s tax bill. Every dollar you contribute to an eligible retirement account reduces the amount of income that you have to pay taxes on.

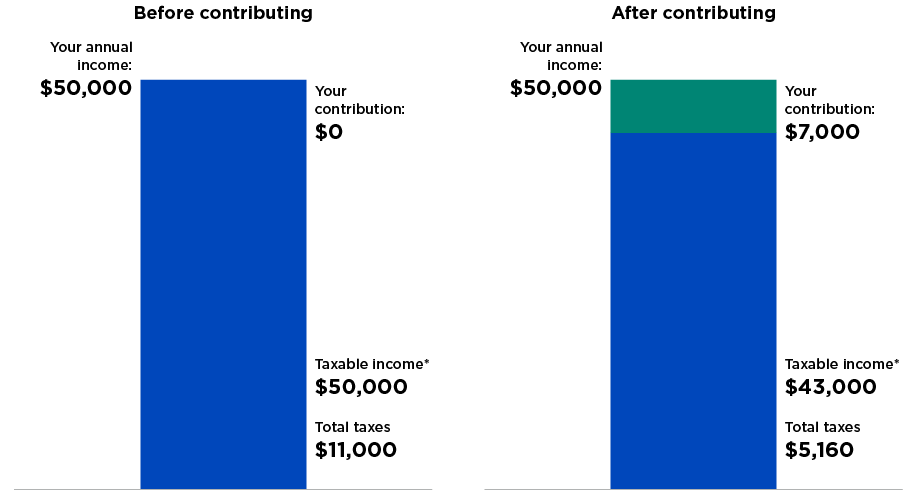

Here’s how it works: You put a portion of your income into a qualified account, such as one your employer offers. If your contributions go in before taxes are taken out, saving for retirement in that account can lower your taxable income.

Let’s say you make $50,000 a year, and you contribute 14% of your pretax income (or $7,000 annually) to your retirement account. Here’s how that would impact your 2024 federal income taxes if you were a single filer using the standard deduction:

In this example, your retirement account contributions reduce your annual income taxes by $840. You benefit by investing in your future and are rewarded with lower taxes today.

There’s another benefit: Typically, the money you put into the account, as well as any earnings your investments make, won’t be taxed until you withdraw it at retirement. If you’re in a lower income tax bracket when you retire, you may be taxed at a lower rate on those withdrawals.

Keep in mind that in some cases, saving for retirement won’t lower your current taxable income. Contributing to a Roth IRA or a Roth account in your retirement plan doesn’t because the money you contribute to this type of account has already been taxed. However, you will not be taxed on the withdrawals or the investment earnings if you’ve owned the account for at least 5 years and are 59 1/2 or older. It’s a trade-off: Investing in a Roth reduces the taxes you’ll pay when you retire, but it doesn’t lower your income taxes today.

*before standard deduction

Enroll in your retirement plan or increase your contributions today.