Market risk

Inflation risk

Interest-rate risk

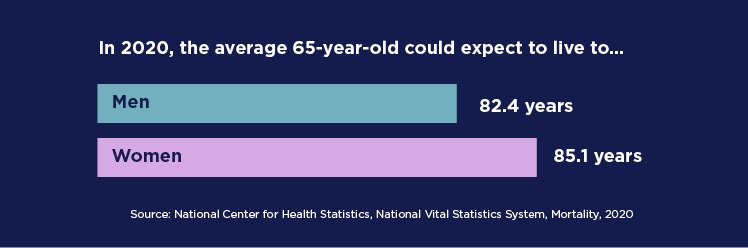

Longevity risk

People today live longer — and many retire earlier — than people in past generations did. In fact, your retirement may last decades. While that may be a good thing, it also means you could outlive your savings, commonly known as longevity risk.

You can reduce longevity risk with careful planning. Consider:

You can't avoid risks, but you can plan for them.

Want to see your current retirement outlook and discuss your plan for financial risks? Use our retirement planning tool and contact your financial professional today.